The Ultimate Guide to GAP Insurance

When buying a new car, there are many different types of insurance policies that you can buy. Of course, you need to get basic insurance cover by law. However, there are a few more options that you can add to give you an even greater and more comprehensive cover.

One type of this optional insurance is GAP insurance. Many people wrongly believe that GAP is just a type of temporary car insurance and isn’t that beneficial. The truth is that depending on your situation, GAP insurance can be a good form of cover that can really help you out if you need to claim.

Here’s a detailed GAP insurance guide to help you better understand GAP insurance, the various types of GAP, and how it could be a good option for you.

Don't Get Stuck Owing: Understanding Gap Insurance

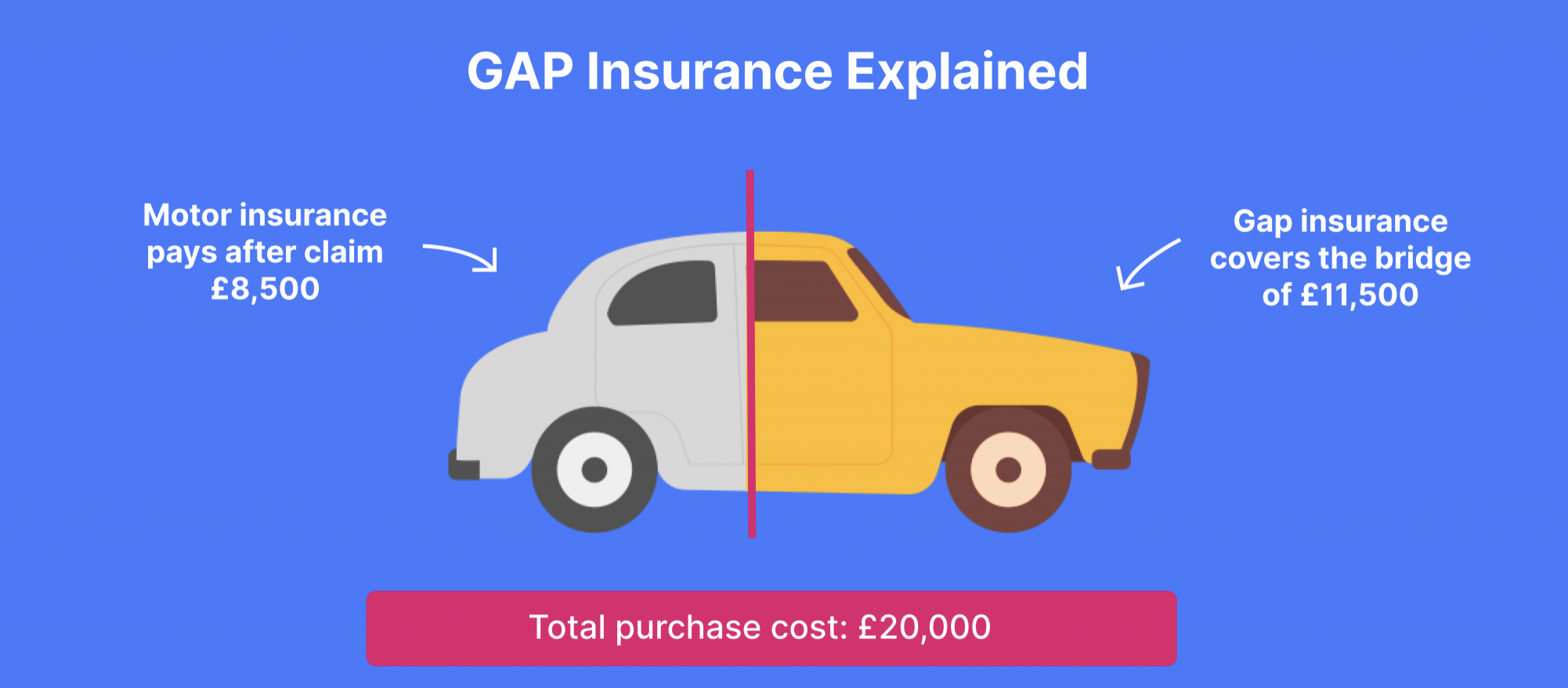

The acronym of GAP stands for Guaranteed Asset Protection. This means that no matter the situation, you will get financial cover if your car depreciates.

When a car is either written off or stolen, or if you need to make any insurance claim to get money to replace the vehicle, most insurance providers will only allow you to claim up to the car’s value at that point.

The issue is that a car’s value decreases massively once you buy it. For example, you can buy a new vehicle for £10,000; a year later, that same car is now worth around £8,500. This means that if that car was written off after a year, you’d only get £8,500, and not the original £10,000 that you bought the car for. As a result of this, you’re effectively losing out on £1,500.

This is where GAP insurance comes in, as it covers this difference in value and allows you to claim that extra cash so that you can replace your old vehicle with something that’s equally as good as it.

GAP insurance is something that’s meant to supplement your current insurance policy and is not a stand-alone option. This means that when you get GAP insurance, you’ll effectively be paying for two policies. Although GAP can cost between £100-£300 for a three-year period, which isn’t that expensive, it can be an additional cost that makes your total amount for insurance pretty high.

In the past, GAP insurance was sold by pushy salespeople and dealerships to get more money out of you. As a result of this, it’s now illegal to be sold GAP insurance at the same time as buying a new car. You’ll usually be offered the opportunity to get GAP a couple of days after buying your vehicle.

GAP insurance will not suit every situation and is mainly designed to help those who have bought or who plan on buying a brand-new car to replace their old one. Your basic car insurance should already have a policy in place where you can get a replacement car of a similar age and condition to the one that was written off or stolen. This makes GAP insurance non-essential, although it can be helpful if you’ve bought your car through a finance deal and would typically owe more than what the insurer gave you without GAP.

Loan, Lease, or Contract Hire? Gap Coverage Explained

You should be aware of the different types of GAP insurance, as each has a fundamental difference that changes the amount and method by which you’re compensated.

Knowing these different types can give you an understanding of how to get the best kind of GAP insurance for your situation, allowing you to get the most out of the scheme. This GAP insurance guide will cover some of the most common types of GAP insurance cover, including the main three that you’re likely to come across.

‘Back to invoice’ GAP insurance

This type of GAP insurance is perhaps the most common type that you’ll come across. This insurance policy pays you the difference between what your insurance provider will give you if your car is written off or stolen and the original amount you bought the car for.

If you don’t currently own the car yet, then the difference will be worked out from the amount you owe to a car finance company.

When looking to get a payout from this type of insurance, you must keep a hold of your invoices and receipts from the initial transaction, as those will be used as proof of how much you bought the car for.

‘Back to value’ GAP insurance

This form of GAP insurance is very similar to the ‘back to invoice’ option, but it’s different enough that you must be careful to choose the right option between the two. This type will give you the difference between how much the car is valued when you’re making a claim on it and how much it was worth when you first bought it. Instead of using how much you paid, the insurance policy looks at the value.

This means that if you bought your car at a good price and less than what it was actually worth, you could get a bit of extra money when choosing this option in the event of an insurance claim.

‘Vehicle replacement’ GAP insurance

This insurance type differs slightly from the ‘back to invoice’ option. With this option, you’ve given the difference between what the insurer will pay you and what you would have paid if you were buying that same car brand-new at that time.

So instead of looking back at how much you paid for the car, you’re instead comparing the value of your current car with how much it would be worth if it was a brand-new vehicle. This only works with new cars, so if you bought a used vehicle, you’d be given the difference between how much you paid for it when you bought it and how much it was worth when it was stolen or written off.

‘Contract hire’ GAP insurance

This type of GAP insurance is only available to those who lease their cars and do not have an option in their contract to buy the vehicle. In this type of insurance, your standard insurance will payout the current value of the car when it was stolen or written off. The GAP insurance will then pay the amount of any remaining payments owed on the lease.

This type of cover protects you from having to pay a lease on a car you’re no longer able to drive, making it a pretty good option if you’re leasing a car.

Are All Cars Covered By GAP Insurance?

Like most insurance policies, there will be exclusions, meaning you may not get a payout if your car meets specific criteria. Plus, there are also situations where you may not get as much money.

Cars that are exempt from GAP insurance include:

- Those that are on a third party or third party, fire, and theft policy

- Those that are worth more than £75,000 at the time of being written off or stolen

- Cars that had done more than 100,000 when the GAP insurance was purchased. This is because cars that have done this mileage are considered to be more likely to break down and be written off due to damages.

- Cars that are older than a certain age. Each insurance provider will have their own maximum age they’ll cover, so be sure to check before comparing the Best GAP Insurance Providers on Car Adviser.

- Cars that are used for hire or taxi services because those vehicles are at greater risk of accidents and wear and tear.

Not only are some cars exempt from getting GAP insurance, but there are also a few circumstances where you won’t be covered for certain things. For example, if your insurance provider deducts from what you’re owed, GAP insurance doesn’t cover this. For example, if you’ve missed a repayment and that’s been deducted from the total amount you receive from your insurance provider, then GAP will not cover this. It only covers the difference between the current value.

Plus, if you’ve made any modifications to your vehicles, such as adding alloys or spoilers, GAP insurance will not cover the cost of these if your car is written off or stolen. This is because when the insurance provider assesses your car’s current value, it will be valuing the car to the specifications it had when you bought it.

It’s also worth clarifying that you must have fully comprehensive car insurance to get GAP insurance payouts. Without this, you won’t be able to get anything, so you must get your main insurance sorted first.

Should I Get GAP Insurance?

As stated earlier in this GAP insurance guide, this type of cover doesn’t suit every situation and individual, and for most, it won’t be an essential purchase. That said, there are some circumstances where getting a GAP insurance policy is a great idea.

Of course, with this type of insurance being optional, you need to weigh the pros and cons and the extra cost to see if it will be worth it. GAP insurance could be helpful if you’re in any of the following situations.

You want to buy a brand new replacement car

Usually, when your car is written off or stolen, your insurance provider will cover the costs to allow you to get a replacement car of the same age and condition. However, in this situation, some people may want to get a brand-new car from a dealership instead. As GAP insurance can give you access to more cash so that you have the value of what your car was worth brand new, you should then have the capital to get a brand-new replacement car.

For example, if you buy a new car for £20,000 and then it’s written off two years later, you’ll get a payout of around £12,000 – it’s value at the time. Although that £12,000 payout should be enough for you to get a similar car to what you were driving, GAP insurance can allow you to recoup that extra £8,000 that was lost in depreciation, allowing you to get a better, brand new car.

You owe money to a car finance company

GAP insurance can be most beneficial for those who have taken out their fiance to get a car. For example, many people take out loans to help fund the outright purchase of a vehicle and then pay that loan back over time.

The issue is that if that car is written off or stolen, you could have to repay a loan for an asset you cannot use anymore. Although you’ll get some money back from your insurer based on what the car is worth at the moment, the total amount of the loan you’ll have to pay back will be the car’s value when you first bought it, which will likely be higher.

Getting GAP insurance in this situation will help as it allows you to earn extra money to help you fully pay off your loan. This helps to protect you more financially.

Situations where you don't need GAP insurance?

Despite there being two good scenarios where GAP insurance is helpful, there are other circumstances where GAP insurance won’t be that helpful and where you should likely avoid it to help you save money.

If you’re considering getting GAP insurance, see if you’re in one of the following circumstances, as it may mean that this type of cover isn’t required and might be an additional cost that isn’t beneficial to you.

You don’t need a brand new car

If you have comprehensive insurance, you’ll get a payout that will allow you to get a replacement car of the same age and condition as your car was when it broke down or was stolen.

This means that even without GAP insurance, you’ll be able to get a new car that’s in good condition. You could save money not having to pay for GAP and still be able to obtain a good quality vehicle. If you’re not concerned about your car’s depreciation, then buying GAP isn’t something you should be concerned about.

You have comprehensive car insurance for a car under a year old

When getting comprehensive car insurance cover, you’ll likely get a feature called ‘new car replacement’. This is where you’ll get a brand new car to replace a stolen or written-off car if it happens within the first year of owning it. Furthermore, some insurance providers extend this period to a full 24 months, meaning that you don’t need GAP insurance if you’re still in this period.

Just be careful with waiting until you buy GAP because if you wait over a year, it means that you won’t be able to get GAP insurance at all. Most providers only allow you to get GAP insurance within 90 days of buying the vehicle. This means that although it won’t be beneficial to claim if your car is written off in the first year, it can be risky not having GAP at all.

You’ve bought a used car

Getting GAP insurance isn’t helpful for most people who have bought a used car. This is because used cars don’t depreciate at the same rate as new cars, meaning that the difference between a used car’s value a year or two after buying it will be minimal.

For example, if you buy a used car for £5,000, it’ll likely still be worth £4,400 after the first year. A new car at the same price can fall to below £3,000 just because of how quickly the value of new cars drops.

GAP can help you recoup smaller amounts on used cars, but for most, this difference will not be that much and may not be worth the cost of adding GAP insurance to your policy.

How to Make a GAP Insurance Claim?

The process of claiming on GAP insurance differs from when you make a claim with regular car insurance.

First, you must get your car insurance provider to declare your car a total loss. This means that it can’t be repaired and will be written off and replaced. Once a total loss is reported, your insurance provider will offer you a claim payment. To get GAP, you can’t accept that payment and must instead contact your GAP provider if it’s not the same as the one giving you regular car insurance.

There’s usually a time limit between getting quoted a claim payment and contacting your GAP provider, so you should do this as soon as possible.

Once contacted, the GAP provider will then process their payment and give you the difference between the valuation of your car and how much you bought for it – if your policy type is ‘back to invoice.

Be aware that GAP payments aren’t automatic, and you need to make a claim and contact them directly. Even if the same provider gives you regular car insurance, you can’t rely on being paid automatically.

GAP Insurance FAQs

How much is GAP insurance?

GAP insurance can cost various amounts based on the condition of your car and the insurance provider you're using. On average, GAP insurance will cost between £100 and £300 for three months. This can be paid in full when you take out the policy annually or monthly over the three years.

It'll likely be cheaper to pay all at once, as you'll probably be charged interest when making monthly payments, although this option can be more affordable as you do not have to make a large payment all at once.

You can by GAP insurance from various places, including car dealerships, banks, finance and leasing companies, and standard insurance providers. Do note that dealers cannot sell you GAP insurance simultaneously when you buy a car and need to wait two days instead.

Can I buy GAP insurance for old cars?

GAP insurance can be obtained for any car you drive, although certain age limits depend on your insurance provider. Most used cars can get GAP insurance; however, doing so may not be the best option for you.

This is because old cars drop in value at a much slower rate than new cars, meaning that the difference between a used car's value when you bought it and when you make a claim may be minuscule, making GAP insurance virtually useless.

How much do cars depreciate in value?

Cars drop in value over the years, meaning a car will never be worth as much as it was when you first bought it. This is why GAP insurance exists, to cover this drop in value.

New cars drop in value at a much faster rate than older cars. The second you drive a new car out of a dealership, its value will drop by 33%. By the end of three years, a car's value will have dropped by a total of 60% of the car's original price. Factors such as the mileage that a car has driven can also impact the drop in value, so cars that have driven more are worth even less.

In comparison, used cars won't drop in value as much from when you purchase them. On average, a used car will drop in value by 33% in its third year, which is much less than the average for new cars. This is why getting GAP insurance for a used or old vehicle isn't worth it, as they retain their value very well.

How long does GAP insurance last?

GAP insurance policies can last between 2 and 5 years, depending on how long you opt for. Once your GAP insurance policy has expired, you'll be able to purchase a new one.

How long does GAP insurance take to pay out?

Payouts from GAP insurance are not instant and may take a few weeks for the payment to go through. On average, this payout can take between 4 to 6 weeks, meaning that if you're using this money to help you finance a brand-new replacement car, you may have to wait a while.

During this period, it's essential to stay in contact with your insurance provider and promptly send over and return any paperwork, as this can speed up the process and make things run more smoothly.